SpaceX filed for its IPO on May 20, 2026. This is one of the most anticipated listings in market history. The S-1 runs to hundreds of pages. We read it so you don’t have to.

Here is everything that actually matters, broken into six chapters.

1. The Numbers: What SpaceX Actually Looks Like Financially

Most people think of SpaceX as a rocket company. The S-1 tells a different story.

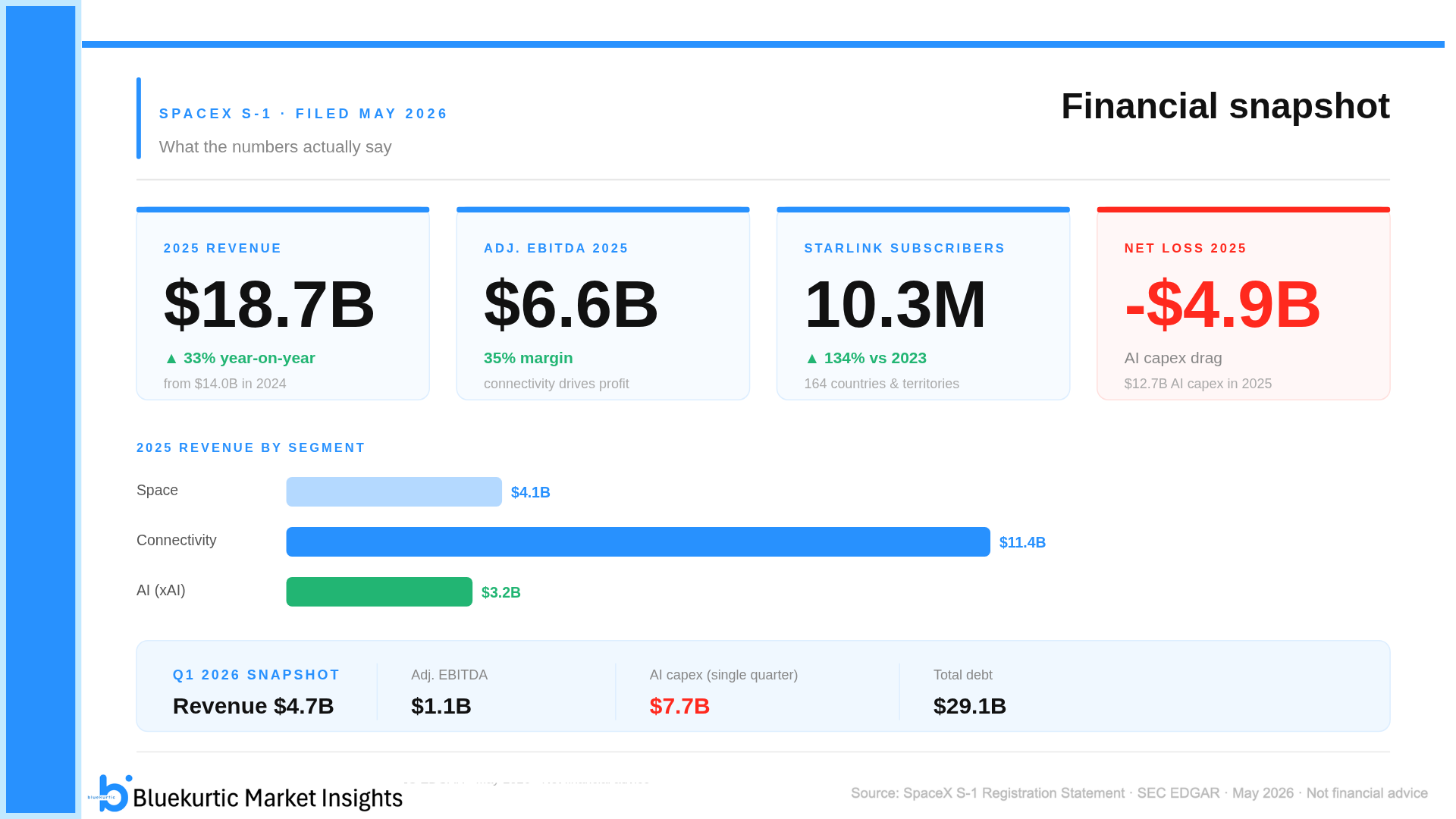

In 2025, SpaceX generated $18.7 billion in revenue, up 33% from $14.0 billion in 2024. Adjusted EBITDA came in at $6.6 billion, implying a 35% margin that most software companies would envy.

But here is the tension buried in those numbers: the company posted a net loss of $4.9 billion in the same year. That is not a sign of a failing business. It is a sign of a company making an enormous deliberate bet on AI infrastructure with $12.7 billion in AI capex in 2025 alone.

In Q1 2026, revenue hit $4.7 billion in a single quarter. The company is accelerating.

The segment breakdown matters too. Connectivity (Starlink) generated $11.4 billion in revenue in 2025 with $4.4 billion in operating income. Space (rockets, launches, Dragon) generated $4.1 billion. AI, which is the newest and lossiest segment, generated $3.2 billion but burned $6.4 billion in operating losses as xAI gets built out.

The profit engine is Starlink. The growth bet is AI. The rocket business funds both.

2. Starlink: The Quietly Dominant Business

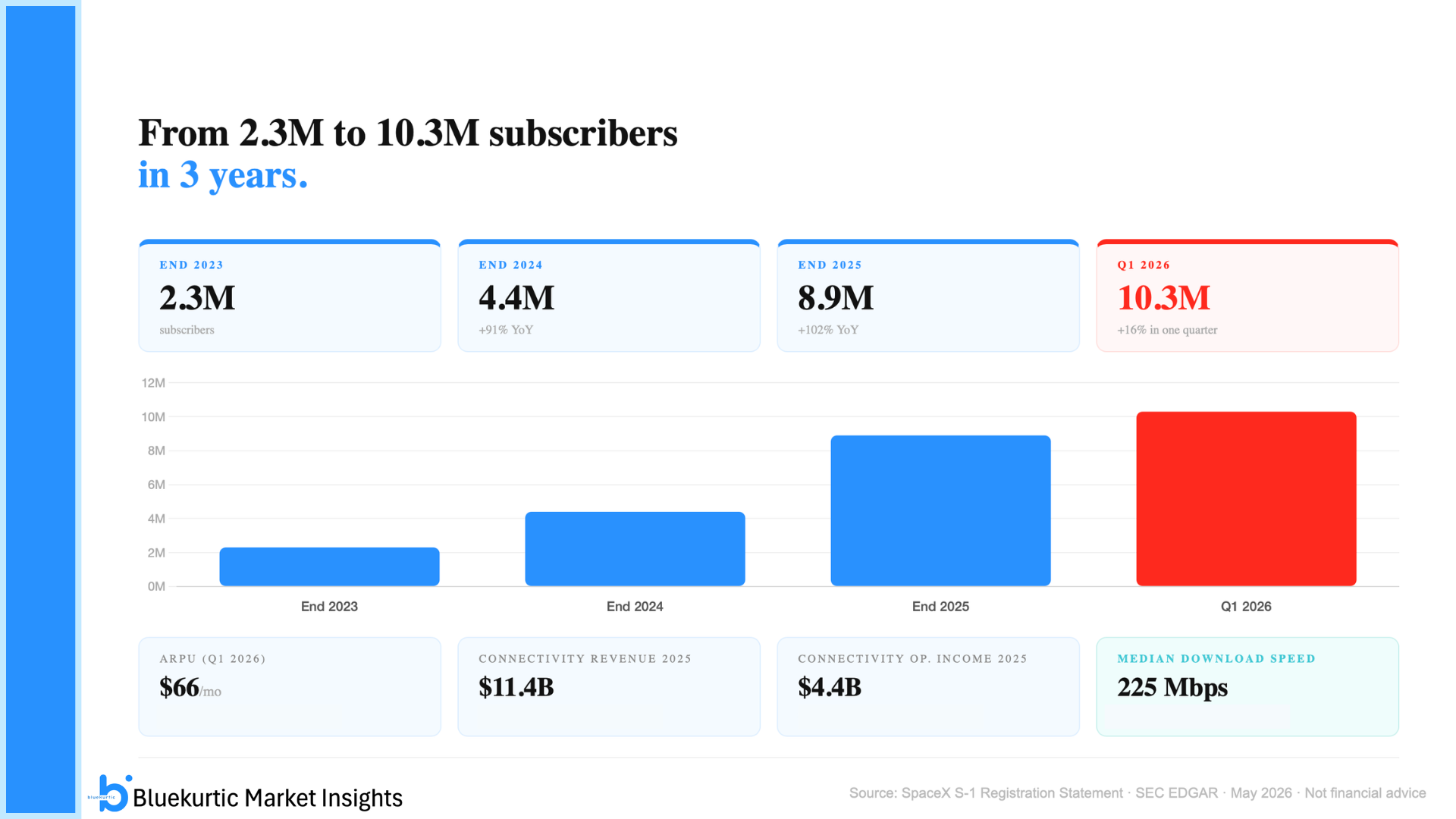

When SpaceX activated Starlink for its first customers in 2020, the satellite internet industry was a graveyard of failed ambitions. Five years later, Starlink has 10.3 million subscribers across 164 countries and territories.

To put that growth in perspective:

- End of 2023: 2.3 million subscribers

- End of 2024: 4.4 million subscribers (+91% YoY)

- End of 2025: 8.9 million subscribers (+102% YoY)

- Q1 2026: 10.3 million subscribers (+16% in one quarter)

Connectivity revenue grew 49.8% year-on-year in 2025. Operating income in that segment grew 120%. Median download speed for residential users sits at 225 Mbps during peak hours.

There is one nuance worth noting: ARPU (average revenue per user) has been declining. It went from $99/month in 2023 to $66/month in Q1 2026. This is not a pricing problem. It is a mix shift. As Starlink expands into emerging markets and enterprise, the per-subscriber revenue average comes down even as total revenue accelerates. Volume is winning over unit economics, which is exactly what you want at this stage.

Starlink alone, as a standalone business, would rank among the top 50 US companies by revenue. It is not a feature. It is a platform.

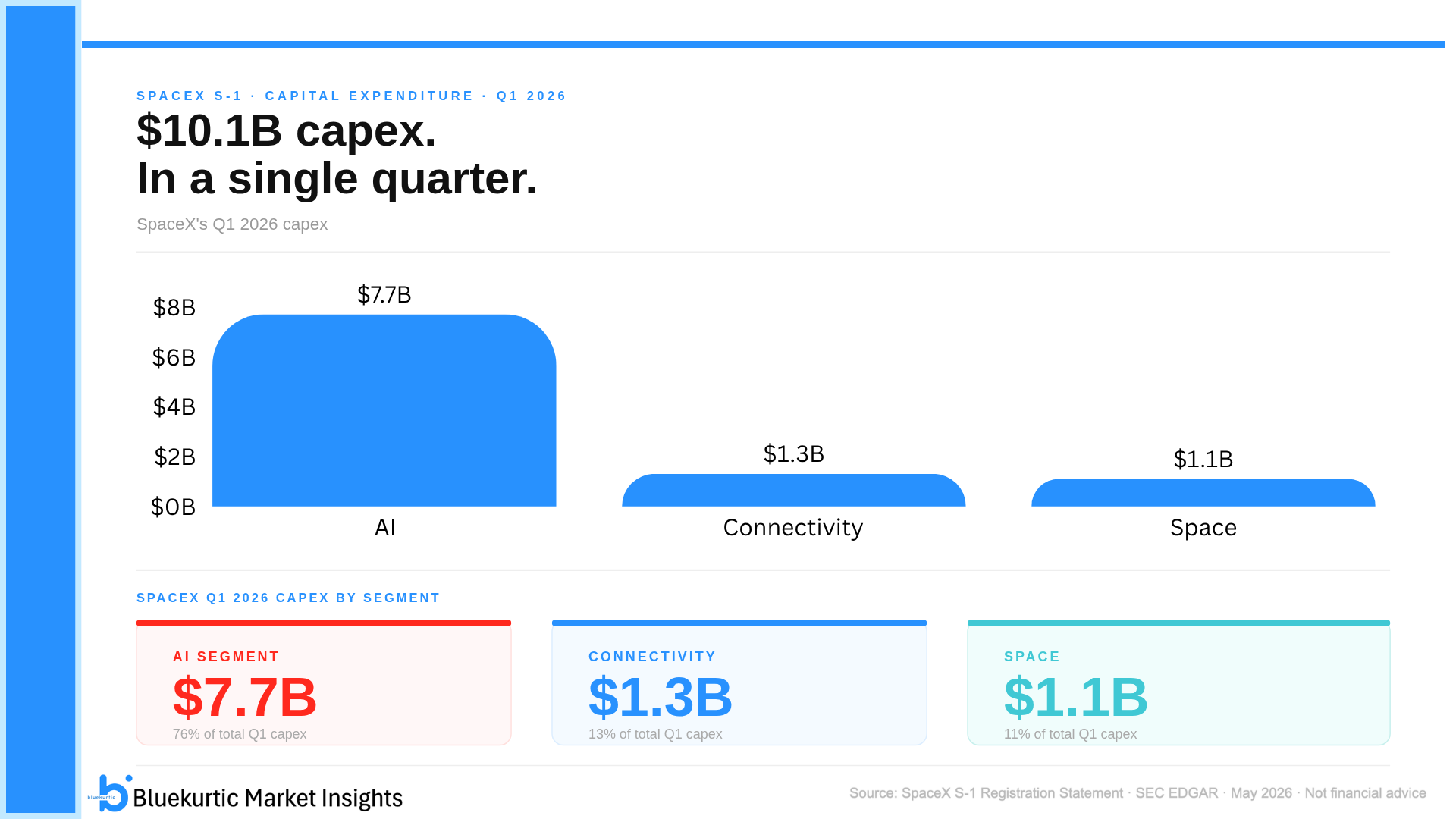

3. The Capex That Should Make Your Eyes Water

SpaceX spent $10.1 billion on capital expenditure in Q1 2026 alone.

Let that land for a moment. One quarter. $10.1 billion.

Of that, $7.7 billion went to the AI segment for building data centres, acquiring GPUs, and scaling the COLOSSUS and COLOSSUS II compute clusters. Connectivity accounted for $1.3 billion (satellites, ground stations, user terminals) and Space took $1.1 billion (Starship development, launch infrastructure).

For context, many of the world’s largest technology companies spend less than that in an entire year on capex. SpaceX is doing it in 90 days.

This is what a genuine infrastructure arms race looks like from the inside. The company is not optimising for near-term profitability. It is buying position in what it believes will be the defining infrastructure market of the next decade: AI compute at planetary and eventually orbital scale.

The risk is obvious. If the AI compute buildout does not generate returns, these losses compound quickly. Total debt as of March 2026 stood at $29.1 billion. This is a high-conviction, high-stakes bet.

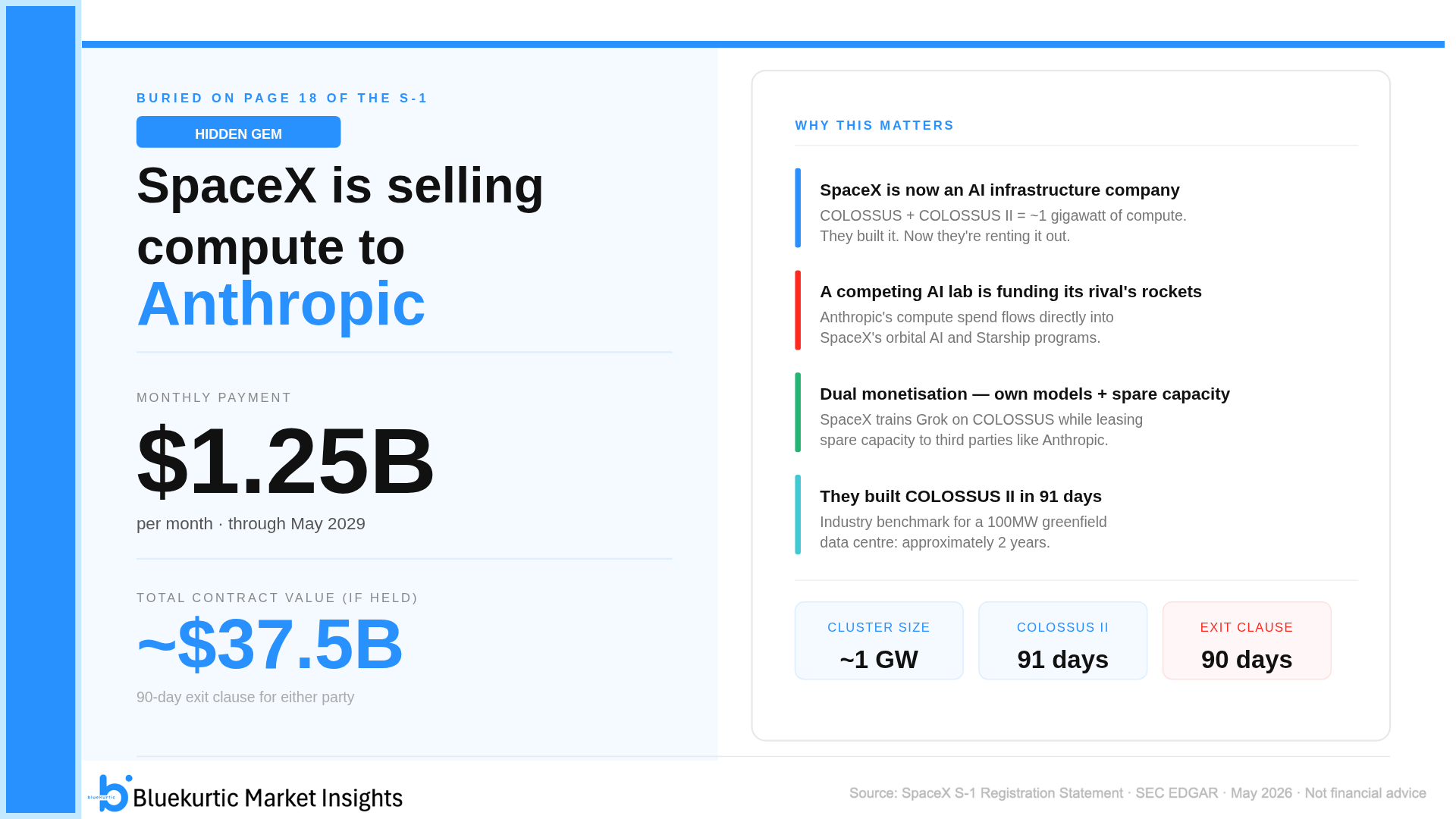

4. The $1.25 Billion Per Month Deal Buried on Page 18

This is the detail most coverage missed entirely.

In May 2026, just weeks before the S-1 was filed, SpaceX signed Cloud Services Agreements with Anthropic, the AI research company and maker of Claude.

The terms: Anthropic pays SpaceX $1.25 billion per month for access to compute capacity across COLOSSUS and COLOSSUS II. The agreement runs through May 2029. If held to term, that is approximately $37.5 billion in contracted compute revenue.

Either party can exit with 90 days’ notice, so it is not a hard obligation. But the existence of the deal reveals something important about SpaceX’s strategy that the headline numbers obscure.

SpaceX is not just building AI infrastructure for its own models. It is becoming an AI compute landlord by training Grok on its own clusters while renting spare capacity to the highest bidder. The irony is hard to miss: a rival AI lab is directly funding the rockets, satellites and orbital AI ambitions of its competitor’s infrastructure provider.

This dual monetization model that own models plus third-party compute leasing gives SpaceX multiple paths to return on its enormous capex. It also raises the question of how many more agreements like this exist or are being negotiated.

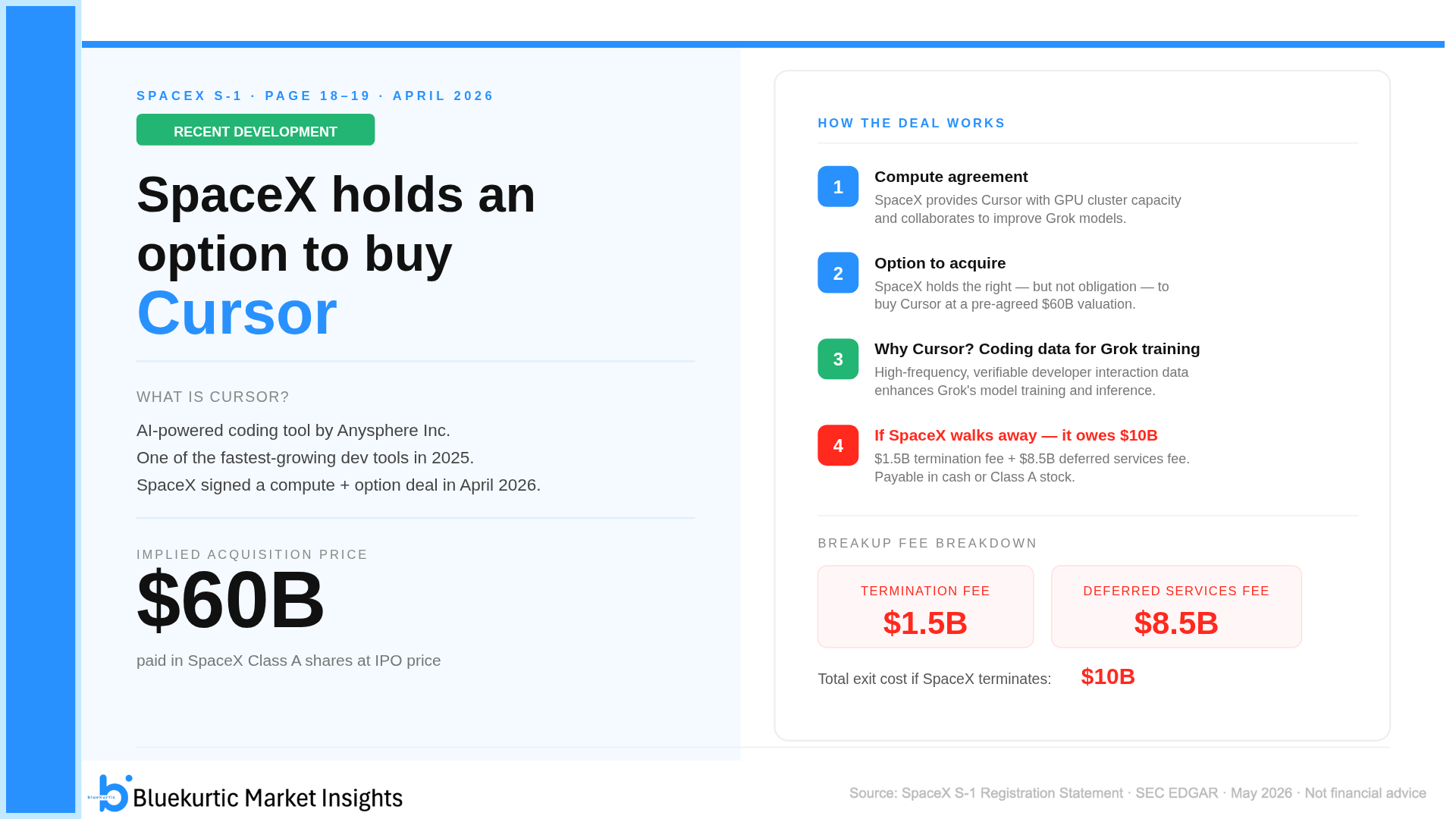

5. The Cursor Deal: Buying the AI Stack One Option at a Time

In April 2026, SpaceX entered into a compute and option agreement with Anysphere Inc., the company behind Cursor, one of the fastest growing AI coding tools in the developer market.

Under the deal, SpaceX provides Cursor with GPU cluster compute capacity and the two companies collaborate on model development, including improvements to Grok. SpaceX also holds an option but not an obligation to acquire Cursor at a predetermined price implying an equity value of $60 billion, paid in SpaceX Class A shares at IPO price.

Why Cursor? The S-1 is explicit about this. Developer interaction data, coding prompts, iteration cycles, architecture decisions, is among the highest quality training data available for AI models. It is structured, verifiable and generated at high frequency by expert users. Feeding that into Grok training is strategically valuable in ways that general web data simply is not.

The twist is in the exit terms. If SpaceX decides to walk away from the option, it owes Cursor a $1.5 billion termination fee plus an $8.5 billion deferred services fee. A total of $10 billion. That is a meaningful commitment for a company that has not yet completed its IPO.

SpaceX is not just building rockets and satellites. It is systematically assembling an AI stack: compute infrastructure, frontier models, real time data from X, and now developer tooling through Cursor.

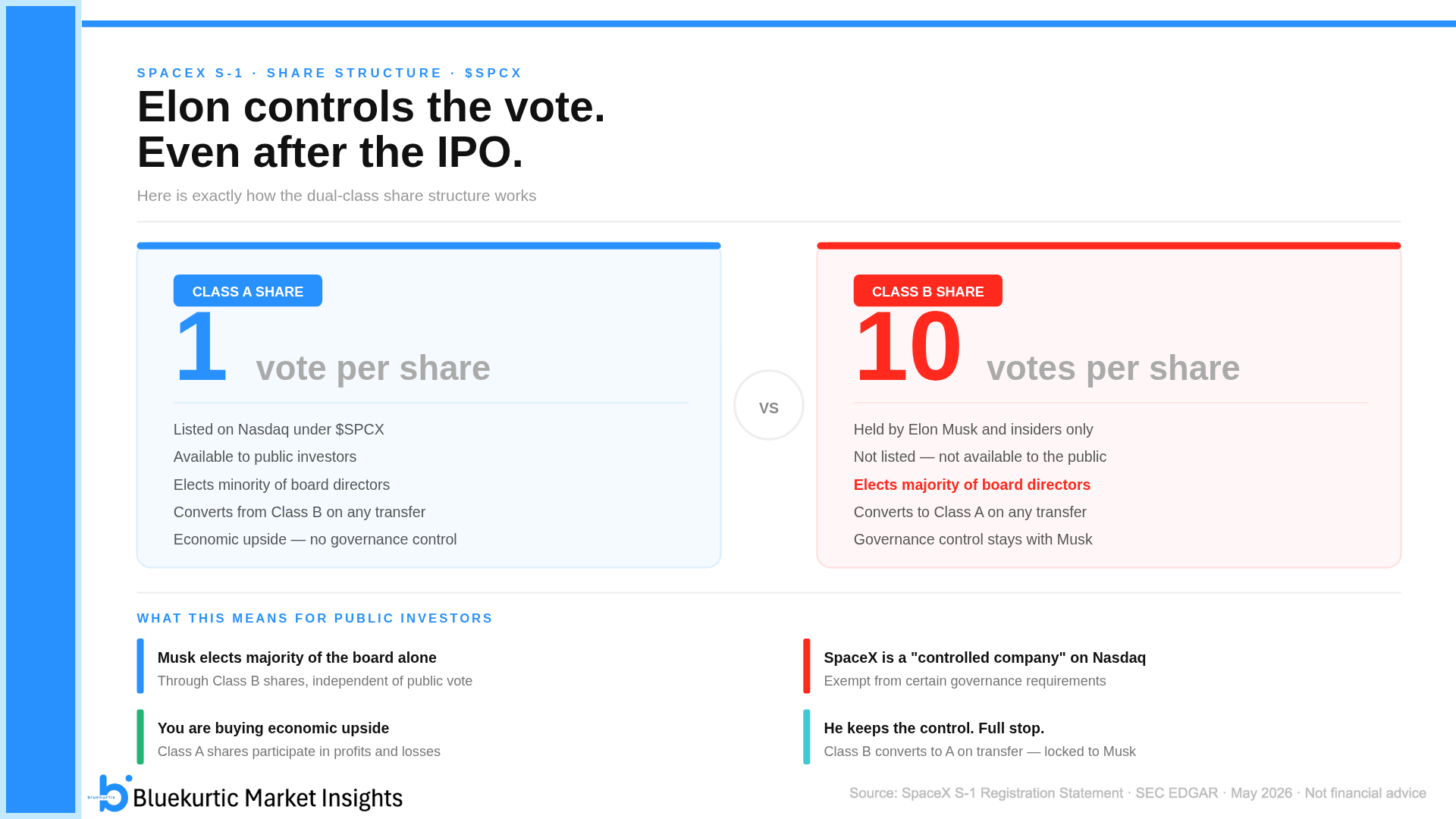

6. Before You Buy SPCX, Understand Who Actually Controls It

SpaceX is going public under a dual class share structure. This is the part of the S-1 that deserves the most careful reading before any investment decision.

Class A shares: the ones available to public investors carry 1 vote per share. These are listed on Nasdaq and Nasdaq Texas under the ticker SPSX.

Class B shares: held by Elon Musk and certain insiders carry 10 votes per share. They are not listed publicly. They convert to Class A on any transfer, which means the super voting power is locked to Musk personally for as long as he holds them.

The practical consequence: Musk holds the right to elect a majority of the board of directors through his Class B shares alone, independent of what Class A shareholders vote. He also controls the outcome of effectively all other shareholder votes for as long as he holds a majority of the combined voting power.

SpaceX will be a “controlled company” under Nasdaq listing rules post-IPO, which means it is exempt from certain corporate governance requirements that apply to other listed companies including the requirement to have a majority independent board and independent compensation and nominating committees.

This does not make SpaceX uninvestable. Many of the best performing public companies of the past two decades like Meta, Alphabet, Snap have operated with dual class structures. But it does mean that as a Class A shareholder, you are buying the economic upside of the business. The governance control stays with Musk. That is the deal, and it is worth understanding clearly before you participate in the IPO.

Final Take

SpaceX is one of the most genuinely unusual companies ever to go public. It operates across rocket launches, global satellite internet, AI compute infrastructure, social media, and frontier AI model development. All under one roof, all vertically integrated, all built on the same engineering first culture.

The S-1 makes clear that the company is in aggressive investment mode. Losses are large and intentional. The bets are enormous and long dated. The control structure concentrates power in one person.

But the underlying businesses, particularly Starlink, are real, profitable and growing fast. And the vision, whatever you think of its probability, is unlike anything else being attempted in the public markets.

SPCX is not a stock. It is a thesis. Make sure you understand which one you are buying.

Source: SpaceX S-1 Registration Statement · SEC EDGAR · Filed May 20, 2026

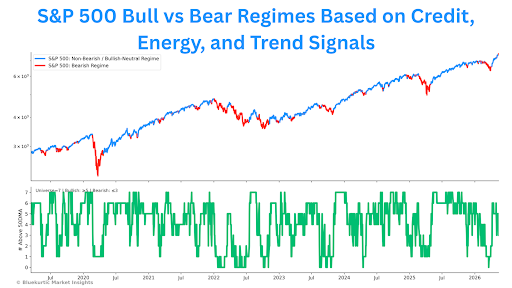

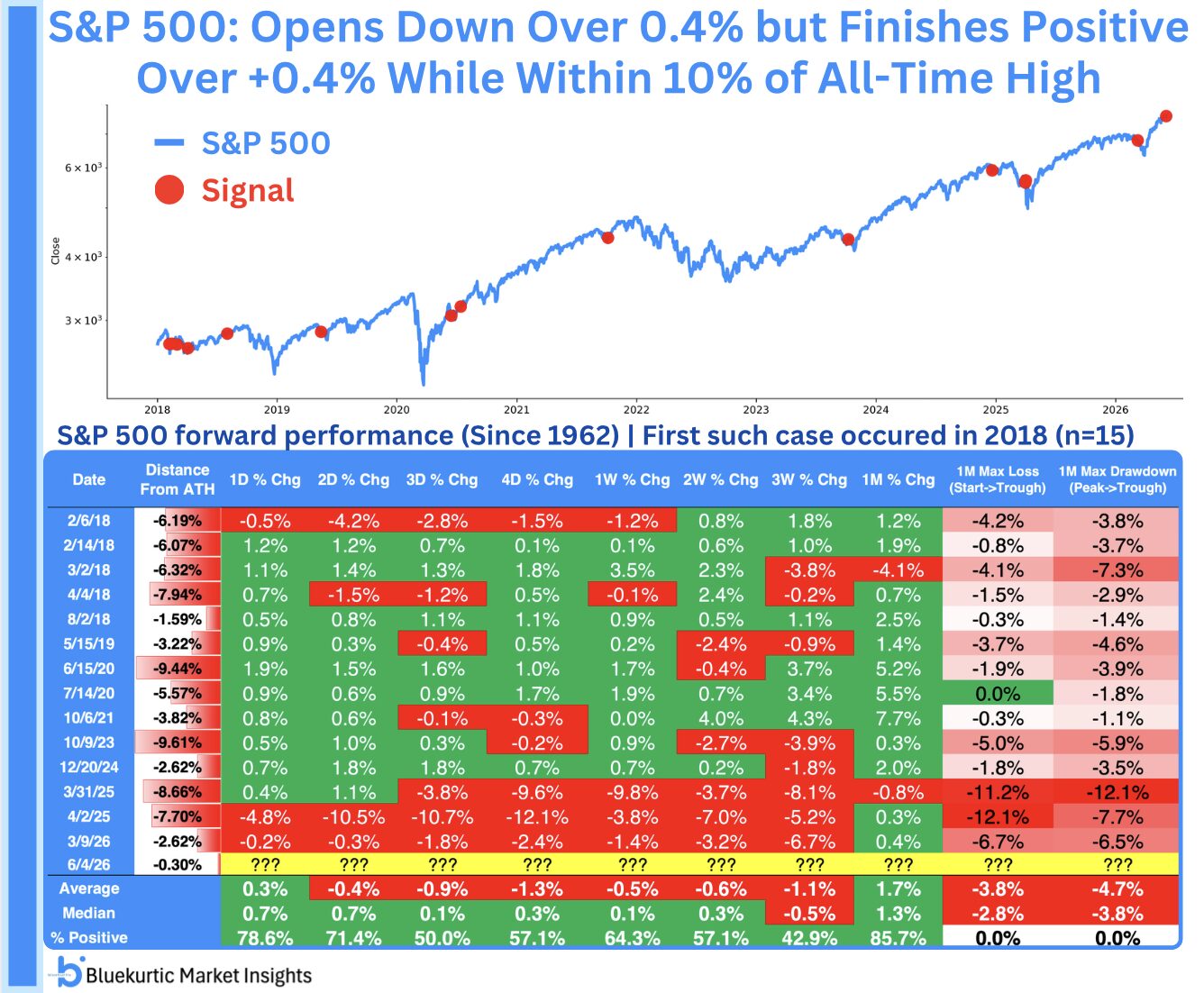

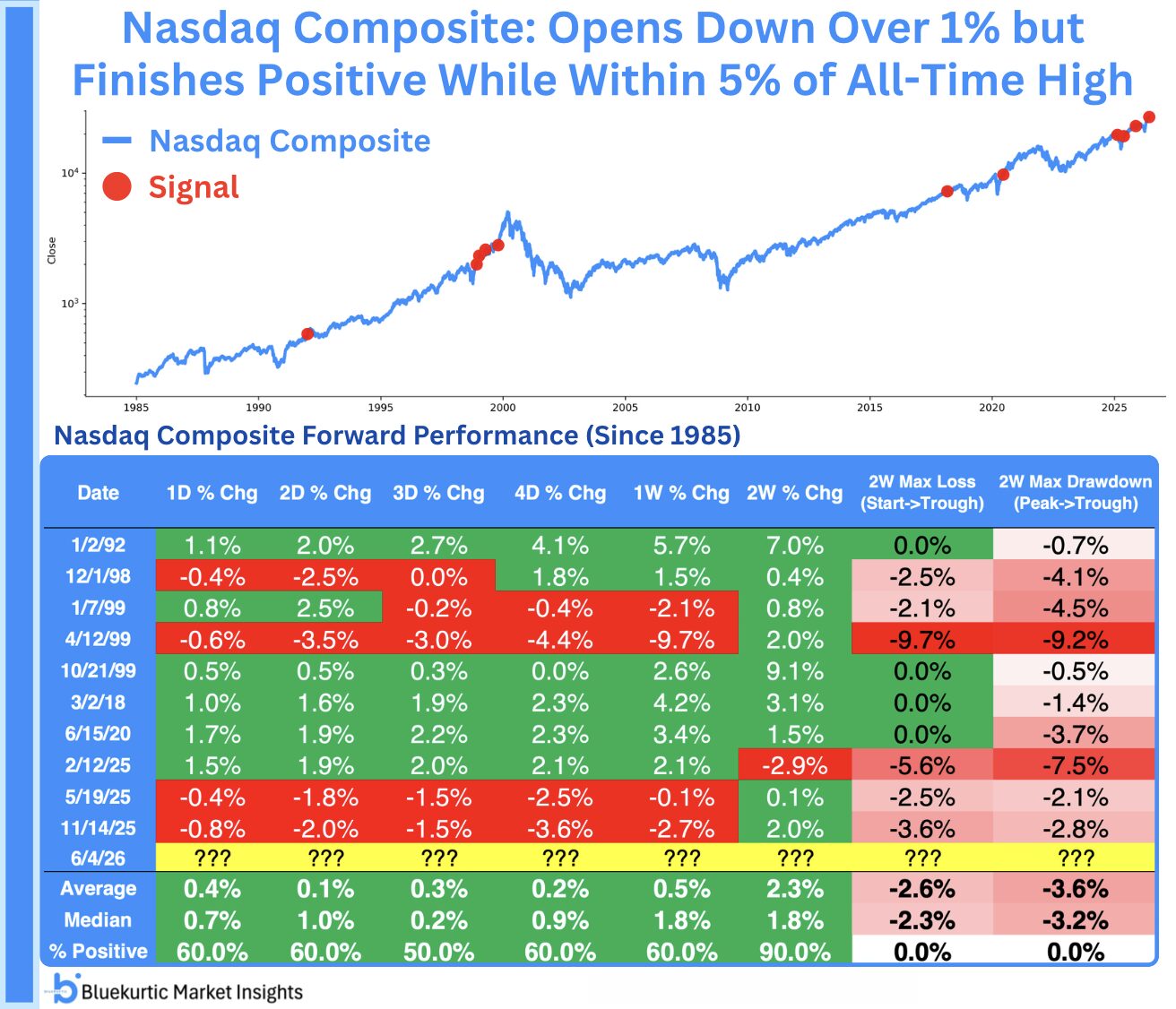

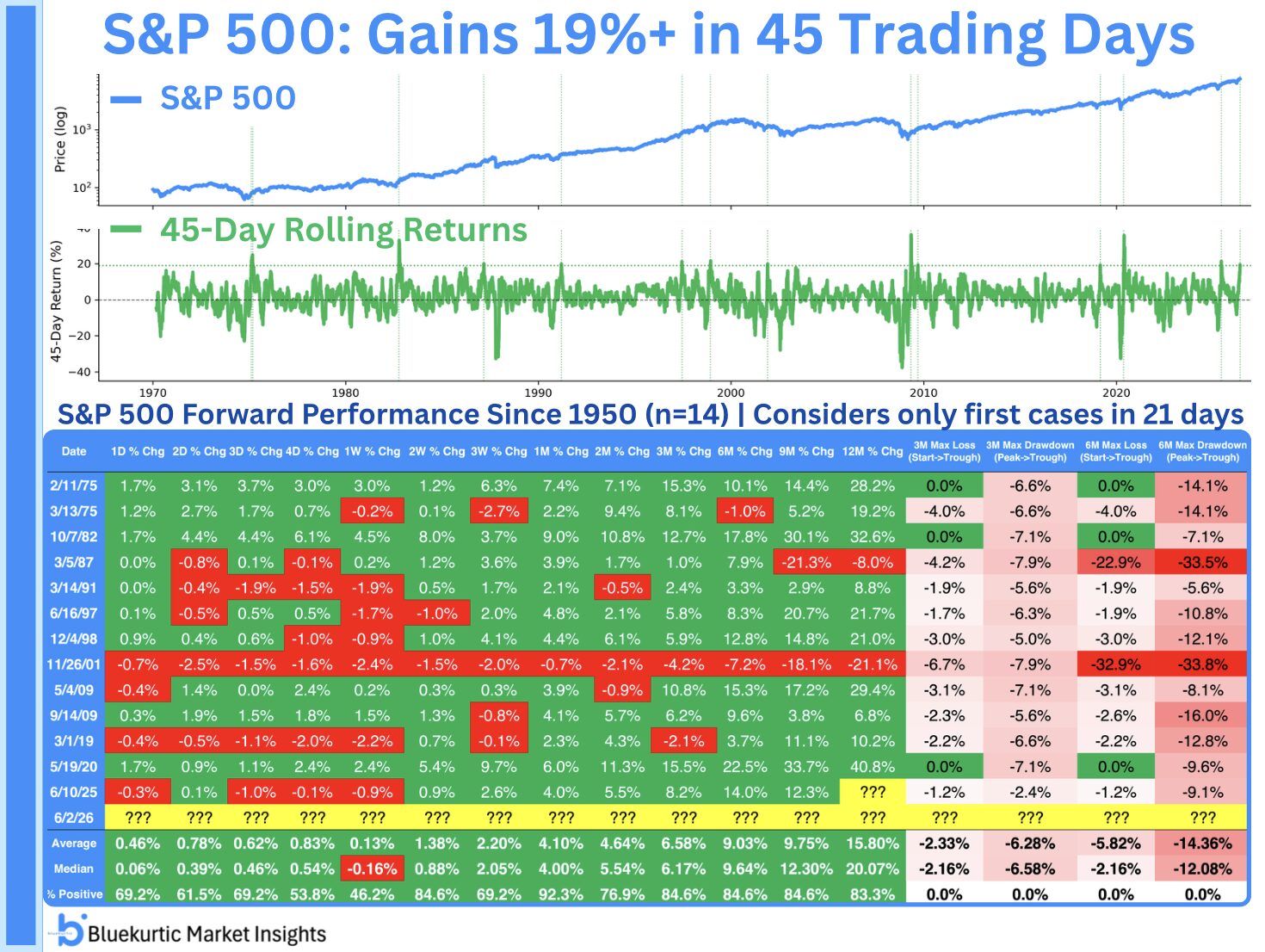

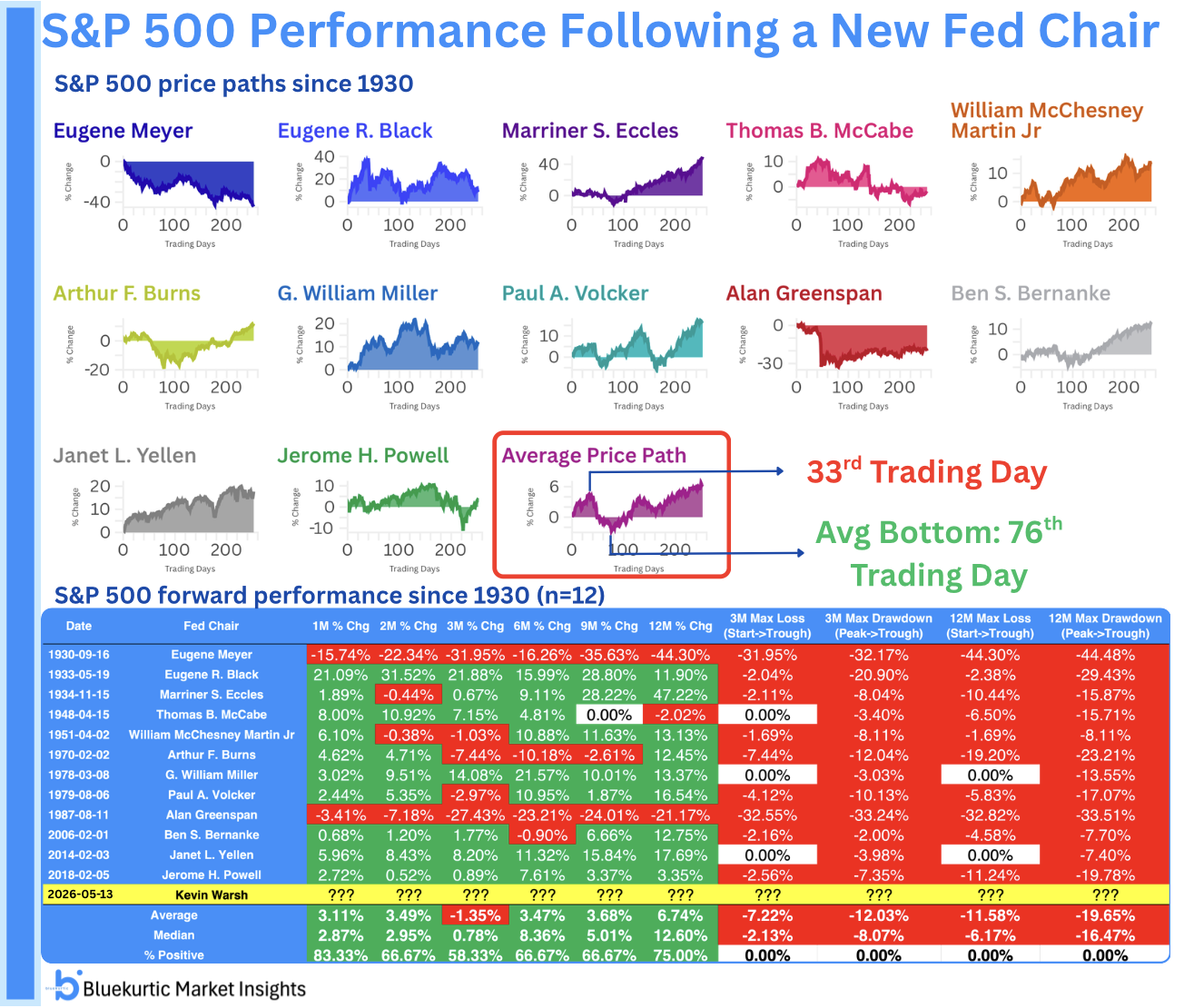

The U.S. Senate has confirmed Kevin Warsh as the next Chair of the Federal Reserve, marking one of the most closely watched leadership changes at the central bank in decades.

The confirmation came through a tight 54–45 vote, the narrowest margin ever for a Fed Chair. That alone highlights how politically charged this transition is, and why there is heightened focus on the Fed’s independence going forward.

While the policy implications will take time to unfold, history offers a useful framework for understanding how markets tend to behave during such transitions.

What History Says About Market Behavior

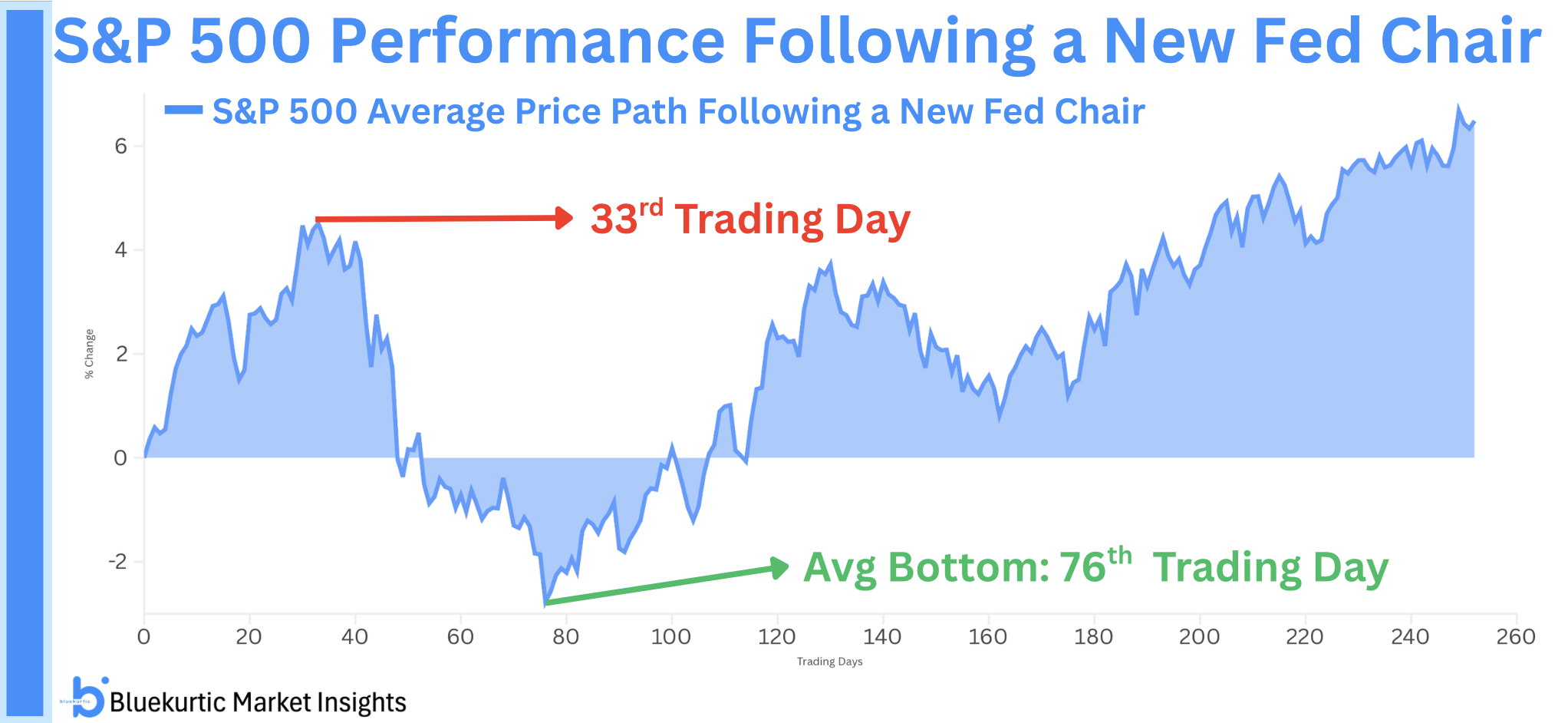

Looking at prior Fed Chair transitions, equity markets have followed a fairly consistent pattern.

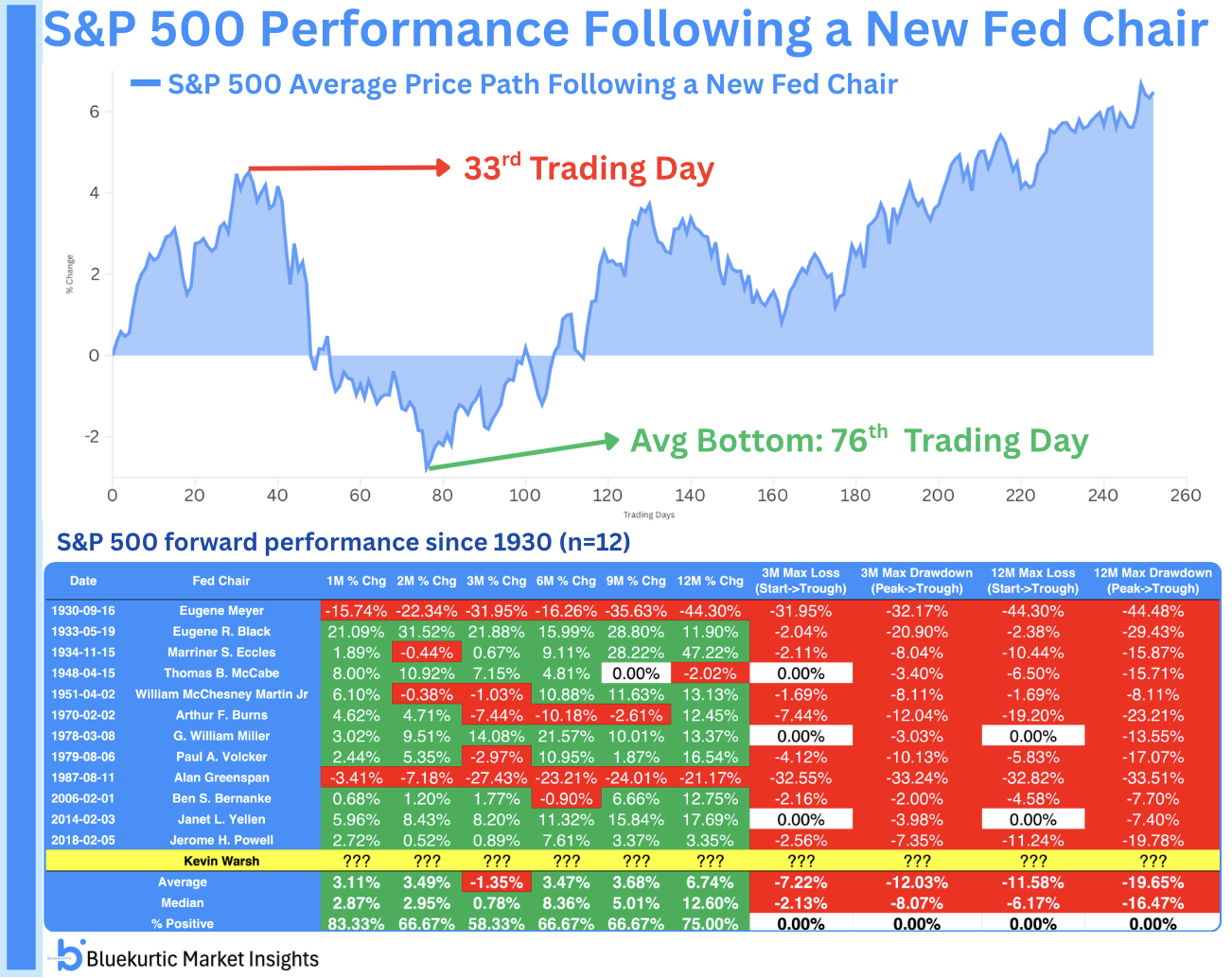

On average, the S&P 500 tends to peak around the 33rd trading day after a new Chair takes office. This is often followed by a period of weakness, with the market typically finding a bottom near the 76th trading day.

Despite this interim volatility, the magnitude of drawdowns has historically been limited.

Across past cycles, the 3-month median maximum drawdown has been just 2.13%. That’s a remarkably shallow decline, especially considering the uncertainty that usually surrounds a leadership change at the Fed.

Across past cycles, the 3-month median maximum drawdown has been just 2.13%. That’s a remarkably shallow decline, especially considering the uncertainty that usually surrounds a leadership change at the Fed.

Short-Term Volatility, But Controlled Risk

The second chart simplifies this pattern by focusing on the average price path.

You can clearly see the tendency for an early rally, followed by a pullback phase, and then stabilization.

This aligns well with the idea that markets initially react to expectations and positioning, before reassessing policy direction as more clarity emerges.

What This Means Going Forward

The combination of a historically tight confirmation vote and a new Fed Chair naturally raises questions about volatility ahead.

However, the data suggests a more nuanced takeaway:

- Yes, volatility may increase in the near term

- But deeper drawdowns have not been typical in past transitions

In fact, the relatively small historical drawdowns support the view that major downside risks tend to be contained, even during periods of policy uncertainty.

Bottom Line

Kevin Warsh’s confirmation sets the stage for an important shift in U.S. monetary policy leadership. The 54–45 voteunderscores just how divided the backdrop is.

But if history is any guide, markets may follow a familiar script—early strength, a mid-phase pullback, and ultimately limited downside risk.

For investors, that suggests staying focused on the broader trend rather than overreacting to short-term volatility.